There are two main ways to receive Medicare coverage, and each offers different benefits.

Original Medicare (Part A and Part B)

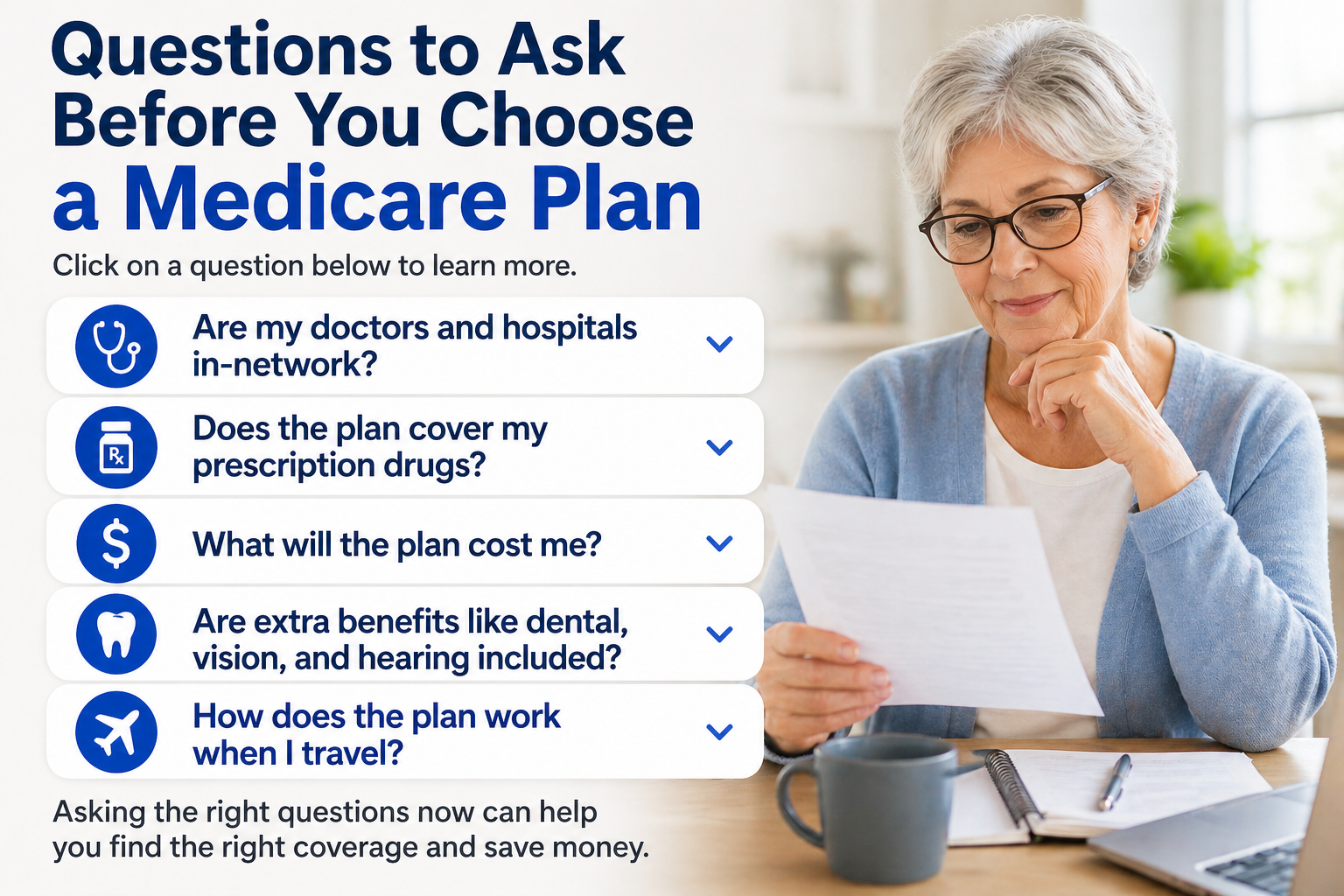

Includes Part A (hospital insurance) and Part B (medical insurance). It allows you to visit any provider that accepts Medicare nationwide, offering flexibility.

However, it does not include dental, vision, or hearing coverage, and you’ll need a separate Medicare Part D plan for prescriptions.

Medicare Advantage (Part C)

Offered by private insurance companies approved by Medicare, these plans bundle hospital, medical, and often prescription drug coverage.

Many plans also include extra benefits like dental, vision, and hearing, but most require you to use a network of doctors and may vary by location.

The best choice depends on whether you prioritize flexibility or bundled benefits.

| Feature | Original Medicare | Medicare Advantage |

|---|---|---|

| Coverage | Hospital (Part A) + Medical (Part B) | Includes Original Medicare + extra benefits |

| Provider Choice | Any provider that accepts Medicare | Network-based (HMO/PPO) |

| Prescription Drugs | Requires Part D | Usually included |

| Dental & Vision | Not included | Often included |

| Travel | Nationwide coverage | Varies by plan |

| Out-of-Pocket Limit | No cap without supplement | Annual max included |

Accessibility

Text size

0

High contrast

Dyslexia-friendly font

Highlight links

Pause animations

Large cursor

Preferences are saved on this browser.

Built for ADA / WCAG 2.1 AA compliance assistance.